Imagine you’re on a medication that keeps your arthritis under control. Your doctor prescribed it, you’ve been taking it for years, and it works. Then your insurance changes - or you switch jobs - and suddenly, they won’t cover your drug unless you try three cheaper ones first. You’re told to fail first before they’ll even consider what your doctor actually recommended. This isn’t a hypothetical. It’s step therapy - and it’s happening to millions of people in the U.S. every year.

What Exactly Is Step Therapy?

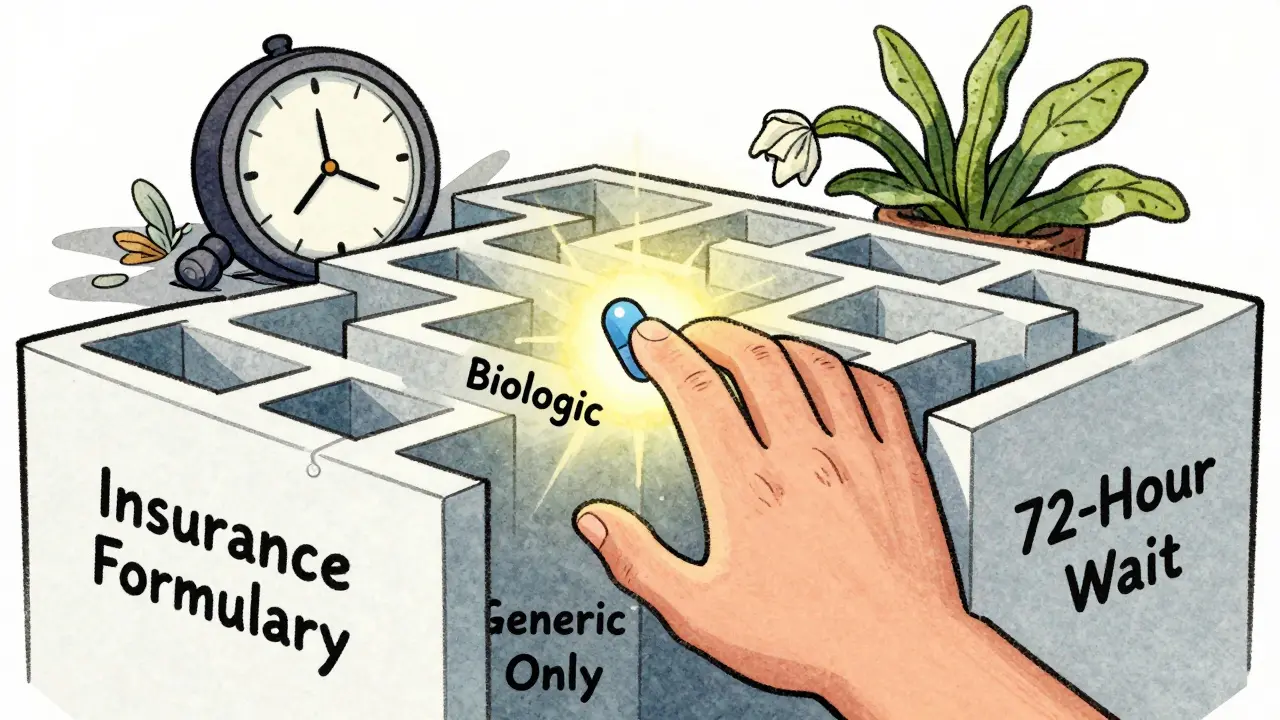

Step therapy, sometimes called a "fail-first" policy, is a rule insurance companies use to control drug costs. Before they’ll pay for a more expensive brand-name drug, they require you to try one or more lower-cost alternatives first - usually generics. It’s not about whether the drug works. It’s about whether it’s the cheapest option on their list. For example, if your doctor prescribes a biologic for rheumatoid arthritis that costs $5,000 a month, your insurer might force you to try three different generic NSAIDs first. Even if you’ve tried them before and they didn’t help - or made you sick - you still have to go through the motions. Only after those fail can you get approval for the drug your doctor actually picked. This isn’t random. Insurance companies organize medications into tiers. Step one is almost always the cheapest, often a generic. Step two might be another generic or an older brand. Step three is the drug your doctor wanted - and it’s the one you’re not allowed to start with.Why Do Insurers Use Step Therapy?

The reason is simple: money. Prescription drug prices in the U.S. are among the highest in the world. Between 2018 and 2023, step therapy adoption rose by 15%, and now about 40% of all drug coverage plans include it. Employer-sponsored plans, Medicare Advantage, and many private insurers use it to cut costs. According to a 2021 Congressional Budget Office analysis, step therapy can reduce pharmaceutical spending by 5% to 15% depending on the condition. That’s billions of dollars saved for insurers - and, in theory, lower premiums for customers. But those savings come at a cost: delayed care. Insurers argue they’re ensuring patients get the most cost-effective treatment. But doctors and patient groups say it’s often the opposite. A 2022 survey by the Arthritis Foundation found that 68% of patients on step therapy experienced worsening symptoms. Nearly half reported disease progression while stuck in the "trial phase."When Step Therapy Can Hurt

The biggest problem isn’t the idea of trying cheaper drugs. It’s the delay. Take chronic pain or autoimmune diseases like lupus or Crohn’s. These conditions don’t wait. Every week you’re on a drug that doesn’t work, your body suffers. Joint damage. Organ stress. Nerve injury. Some of it is permanent. One Reddit user, "ChronicPainWarrior," shared how they spent six months trying three different NSAIDs before their insurer approved a biologic for rheumatoid arthritis. By then, their joint damage had advanced. Surgery was now needed. Another issue? Restarting the process. If you switch insurance - even because you got a better job - you might have to go through step therapy all over again. Even if you’ve been on the same drug for five years. Your new insurer doesn’t care about your history. They only see their formulary. And the appeals process? It’s slow. Blue Cross Blue Shield of Michigan says they review exceptions in 72 business hours. But real-world reports from patients show it often takes 4 to 8 weeks. During that time, you’re not just waiting - you’re getting sicker.

What Are the Exceptions?

You’re not completely stuck. Federal and state laws require insurers to allow exceptions - but you have to ask for them. The Safe Step Act, introduced multiple times in Congress since 2017, outlines five clear situations where insurers must approve your doctor’s original prescription without forcing you to try cheaper drugs first:- The drug you’re currently taking is working and you’re stable on it.

- The required drug has already failed for you in the past.

- The required drug is contraindicated because of another condition or allergy.

- Delaying treatment would cause severe or irreversible harm.

- The required drug would prevent you from doing basic daily tasks.

How to Fight Back

If you’re caught in step therapy, here’s what actually works:- Ask your doctor to file an exception - don’t wait for them to bring it up. Bring the five Safe Step Act criteria with you to your appointment.

- Get everything in writing - your doctor’s note, your medical history, pharmacy records showing prior drug failures. Attach them to the request.

- Call your insurer and ask for a case manager. Ask for the exact name of the person handling your case. Track every call.

- Check your state’s laws. 29 states have passed step therapy protections. Some require insurers to respond within 24 hours for urgent cases. Others mandate that exceptions be granted automatically if you’ve been on the drug for over a year.

- Look into patient assistance programs. Many drugmakers offer co-pay cards or free trials that can bypass step therapy - especially for specialty medications.

Generics Aren’t Always the Answer

It’s easy to assume generics are just as good. And often, they are. In fact, about 90% of prescriptions in the U.S. are for generics. But not all drugs have true equivalents. Some brand-name drugs have unique delivery systems, different inactive ingredients, or specific dosing that generics can’t match. For example, some asthma inhalers have different propellants. Some epilepsy meds have tiny variations in absorption that can trigger seizures. Some antidepressants have side effect profiles that make switching dangerous. Insurers don’t always account for this. Their formularies are built on cost, not biology.What’s Changing in 2026?

Step therapy is growing - not shrinking. Analysts predict it will cover 55% of specialty drug prescriptions by 2025. Self-insured employer plans, which cover about 61% of Americans, are still mostly outside state laws. That means millions have no legal protection at all. The Safe Step Act is still pending in Congress. If it passes, it would force those self-insured plans to follow the same exception rules as fully-insured ones. That could be a game-changer. Meanwhile, more states are tightening their rules. In 2023, eight states added time limits for exception decisions. Some now require insurers to approve requests within 72 hours for chronic conditions. But until federal law catches up, you’re on your own. The system is designed to save money - not to protect your health.Final Reality Check

Step therapy isn’t evil. It’s a tool. And like any tool, it can be used well or badly. When it helps someone find a cheaper, equally effective drug, it’s a win. When it delays life-changing treatment for months - or pushes someone to quit their medication - it’s a failure. The truth? Insurance companies aren’t doctors. They’re businesses. Their job is to manage risk and cost. Your job is to manage your health. That means knowing your rights, asking for help, and never accepting "no" as the final answer. If you’re on step therapy, don’t wait. Start documenting. Talk to your doctor. Call your insurer. And if you’re told you have to fail first - remember: you’re not failing. The system is.What is step therapy in insurance?

Step therapy is a rule used by insurance companies that requires you to try one or more lower-cost medications - usually generics - before they’ll cover a more expensive drug your doctor prescribed. It’s also called a "fail-first" policy because you must prove the cheaper options didn’t work before moving to the next step.

Why do insurers make you try generics first?

Insurers use step therapy to reduce drug costs. Generic medications are significantly cheaper than brand-name drugs. By requiring patients to try them first, insurers save money - sometimes 5% to 15% on certain prescriptions. The goal is to avoid paying for expensive drugs unless absolutely necessary.

Can I skip step therapy if my doctor says I need the brand-name drug?

Yes - but you have to request an exception. Your doctor must submit medical documentation proving one of five criteria: the required drug failed before, it’s contraindicated, delaying treatment would cause harm, you’re already stable on your current drug, or the required drug would stop you from doing daily activities. Approval isn’t automatic - you have to fight for it.

How long does a step therapy exception take to get approved?

Insurers are supposed to respond within 72 business hours for standard requests and 24 hours for urgent cases. But in practice, many patients wait 4 to 8 weeks. Delays happen because of paperwork backlogs, incomplete submissions, or slow communication between doctors and insurers. Always follow up.

What if I switch insurance plans?

You may have to restart step therapy - even if you’ve been on the same medication for years. New insurers don’t recognize your prior history unless you provide proof. Always bring your prescription history and doctor’s notes when switching plans. Some states require exceptions for patients already stable on a drug, but not all do.

Are there laws protecting me from step therapy delays?

Yes - 29 states have passed laws requiring insurers to allow exceptions and set time limits for responses. But these laws usually only apply to fully-insured plans, not self-insured ones (which cover about 61% of Americans). Federal law doesn’t yet require the same protections for self-insured plans, though the Safe Step Act is working to change that.

Can I get help paying for the drug while waiting for approval?

Many drug manufacturers offer patient assistance programs, co-pay cards, or free trial programs that can cover your medication while you wait for insurance approval. Ask your pharmacist or check the drugmaker’s website. These programs often bypass step therapy rules entirely.

What should I do if my step therapy request is denied?

Appeal the decision in writing. Request a formal review from your insurer’s appeals department. Include all medical records and a letter from your doctor explaining why the step therapy requirement is harmful. If the appeal is denied, you can contact your state’s insurance commissioner’s office - they can intervene on your behalf.

10 Comments

Susie Deer January 14, 2026

Insurance companies are just profit machines pretending to care about you

They don't give a damn if your joints turn to dust as long as their quarterly numbers look good

Step therapy is corporate cruelty dressed up as cost control

Alvin Bregman January 16, 2026

i get why they do it but its messed up when youve been on the same med for 5 years and now you gotta start over

my buddy had to wait 3 months for his biologic after switching jobs

by then his knees were shot

its not about savings its about bureaucracy winning

Robert Way January 17, 2026

why do people think generics are the same

theyre not

my asthma inhaler has a different propellant and i had panic attacks

insurers dont care about biology they care about the price tag

and doctors are stuck doing paperwork all day instead of treating people

Sarah Triphahn January 17, 2026

you people are so dramatic

if you cant afford the drug then you shouldve planned better

the system works fine if you just follow the rules

its not the insurers fault you didnt read your policy

and stop acting like youre being persecuted

its just business

Allison Deming January 18, 2026

It is profoundly troubling that we have allowed corporate entities to dictate medical treatment decisions that should be made solely by clinicians and patients based on individualized clinical judgment

The commodification of healthcare has reached a point where human suffering is reduced to actuarial tables and profit margins

When an insurance company determines that your pain is not urgent enough to warrant timely access to a prescribed medication, we have crossed an ethical threshold that should not be crossed in a civilized society

TooAfraid ToSay January 20, 2026

what if this is all a ploy by big pharma to keep prices high

what if generics are actually better and the doctors are being paid off

think about it

why would they make you try cheaper stuff first unless they knew the expensive one was overhyped

theyre all in on this scam

Dylan Livingston January 20, 2026

Oh sweet summer child

You think this is about health

Its about the quiet genocide of chronic illness sufferers

They dont want you well

They want you docile

They want you on a $10 pill that barely works so you dont complain too loudly

And when you finally collapse from organ failure

Theyll say you shouldve tried harder

Pathetic

Andrew Freeman January 21, 2026

my insurance made me try 4 generics for my migraines

one gave me hives

one made me suicidal

one did nothing

the last one gave me diarrhea for a month

then they approved my real med

took 11 weeks

by then i lost my job

and my dog

and my will to live

but hey at least they saved 50 bucks

says haze January 22, 2026

The structural absurdity of step therapy reveals a fundamental epistemological failure in American healthcare

It assumes that cost equivalence implies therapeutic equivalence

But biology is not a spreadsheet

Pharmacokinetics cannot be optimized by algorithm

And human suffering does not respect actuarial risk models

What we are witnessing is not policy

It is the institutionalization of medical nihilism

Sarah -Jane Vincent January 22, 2026

They're watching you

They know you're on that biologic

They're tracking your prescriptions

They're waiting for you to slip up

Next thing you know your meds will be denied again

They're building a database of chronic illness patients to target later

They want to force you off everything

And then when you're too sick to work

They'll cut your disability

It's all connected

Don't trust them

Save every email

Record every call

They're coming for you